By Mengdi Yue and Yiyuan Qi

Chinese loans to Africa are down once again, but not out. Boston University Global Development Policy Center’s newly updated Chinese Loans to Africa (CLA) Database shows that, despite a slight rise in 2023, Chinese loan commitments to Africa fell again to $2.1 billion in 2024, a 46% drop from the previous year. New loan commitments in 2024 went to just six projects in five African countries, far below the peaks of the 2010s.

These new data indicate China’s continued strategic shift from large-scale lending to selective engagement in resilient sectors such as transportation, energy transmission, water, and financial services, and targeting borrowers that have established track records and strong project fundamentals.

From 2000 to 2024, Chinese loan commitments to Africa totaled $180.87 billion, across 1,319 loans and covering 49 African states as well as seven regional institutions. Most of them were from the Export-Import Bank of China (CHEXIM) and the China Development Bank (CDB), and others from commercial banks and Chinese companies and state-owned enterprises.

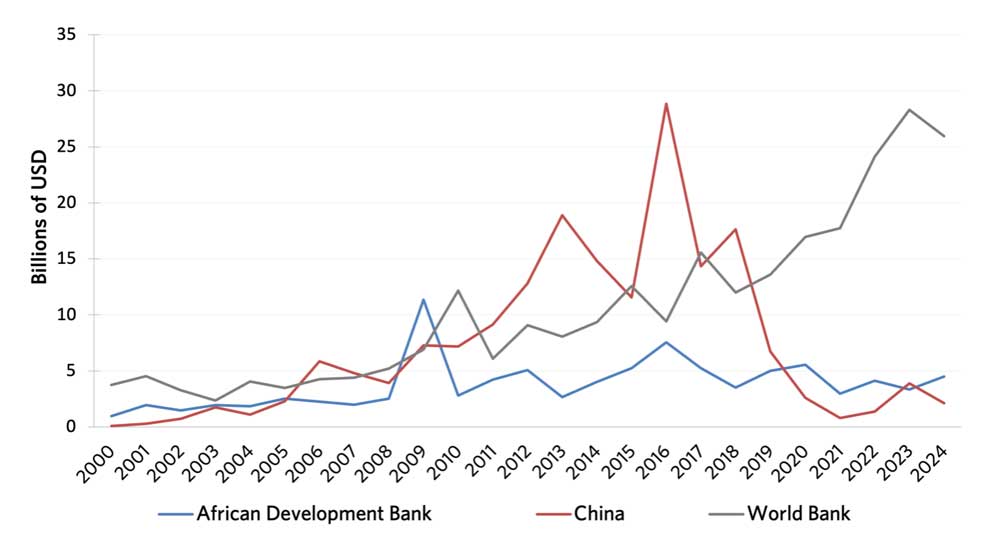

Compared with loan commitments from the World Bank and African Development Bank, China’s loan commitments to Africa grew quickly after 2000 and exceeded the World Bank in most of the years between 2011 and 2018. After 2018, they declined dramatically and have remained below $5 billion, about the same level as the African Development Bank.

Back to Basics: Sectoral Concentration

The 2024 financing portfolio concentrated exclusively in four sectors: transportation ($1.2 billion across three road or transport infrastructure projects in the Democratic Republic of the Congo (DRC), Kenya and Angola), energy ($760 million for an electricity transmission line in Angola), water and sanitation ($85 million for rural well drilling in Senegal), and financial services ($76.5 million to Egypt’s National Bank for local small and medium-sized enterprise (SME) support).

This concentration does not signal a renewed focus on these sectors but reflects their greater resilience to attract financing even as overall lending contracts—partly because they are critical social welfare infrastructure that face challenges securing equity investment.

Notably absent were new commitments in information and communication technology, industry, trade, or other sectors that previously received substantial Chinese financing. In the energy sector, China has not financed new fossil fuel projects since 2020 But lending to renewable energy such as solar and wind has also remained limited, as China increasingly channels clean energy support through foreign direct investment and equipment trade rather than sovereign loans.

A Smaller Cohort of Strategic Partners

Only five countries received new Chinese loan commitments in 2024: Angola, Kenya, the DRC, Senegal, and Egypt. Three of these—Angola, Kenya, and Egypt—rank among the continent’s largest borrowers from China historically, together accounting for over one-third of all Chinese lending to Africa since 2000.

Yet established partnerships don’t necessarily mean lower risk: according to IMF’s World Economic Outlook, interest payments in 2024 consumed 72% of Egypt’s government revenues, 31% of Kenya’s, and 27% of Angola’s. That is well above the roughly 20% level that S&P Global has linked to heightened sovereign default risk.

China’s willingness to continue lending to these fiscally strained partners demonstrates the importance of relationship continuity and patient capital even amid fiscal challenges of borrowers.

The RMB Turn: New Currency Dynamics

An emerging trend is the growing use of RMB-denominated lending. All the new loans to Kenya in 2024 were RMB-denominated at 4% interest rate and were issued as export buyer’s credit. Between 2000 and 2024, Kenya received approximately $2.4 billion in RMB-denominated loans with an average interest rate of 2.97%, funding projects across the energy, transportation, ICT, health, education, mining and public administration sectors.

In October 2025, Kenya converted an estimated $3.5 billion of its Standard Gauge Railway debt from dollars to yuan. The move lowers interest costs and reduces dollar dependence, but creates new potential currency risks.

Looking Ahead: Diversification but Not Replacement

China’s financial engagement in Africa is developing a more diverse toolbox and becoming less reliant on sovereign debt, with growing emphasis on risk mitigation, market mechanisms, and RMB-based lending. This recalibration offers African governments opportunities to pursue development without continued debt accumulation. It also gives China opportunities to better align with each country’s strategies and development goals, especially in energy transition areas.

However, trade and investment cannot replace loans, especially for already indebted countries. Increasing pressure to repay existing debt, combined with the lack of new lending, might lead to prolonged inaction on tackling climate change. Africa still faces a large shortfall in infrastructure funding, and the sectors that received loans in 2024 represent areas where market mechanisms have not been able to meet financing needs.

The real test is how China’s financial engagement in Africa can still remain impactful as lending scales down and grows more selective. How China manages the trade-offs of a lower-lending era while maintaining its partnerships will shape not only the future of China-Africa relations but also the broader trajectory of green growth in the Global South.

Mengdi Yue is an independent researcher specializing in sustainable finance and China’s overseas investment and yiyuan qi is a Research Fellow at the Boston University Global Development Policy Center (GDP Center)