By Mengdi Yue

China and Africa’s economic relationship has continued to evolve over the last decade. Recent milestones include the ten partnership actions announced at the 2024 Beijing Summit of the Forum on China-Africa Cooperation, the Green Mining and Minerals Initiative launched at the 2025 Johannesburg G20 summit and China’s most recent expansion of its zero-tariff access across the continent.

New research from the Boston University Global Development Policy Center and the African Economic Research Consortium maps out the economic trends underlying these commitments. The study collects most recent data available on China’s engagement in African countries across trade, foreign direct investment (FDI) and lending.

Extractives Still Drive Africa’s Export Growth to China

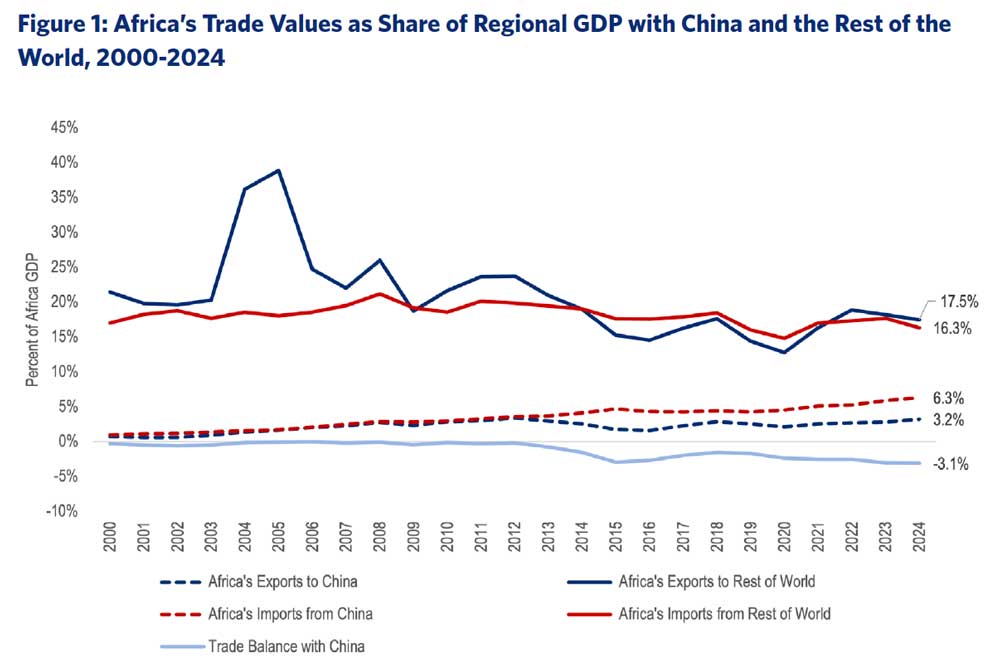

Africa’s bilateral trade with China reached a record $275 billion in 2024, consisting of $182 billion in imports (6.3% of regional GDP) and $93 billion in exports (3.2% of regional GDP). Both imports and exports grew since 2023, even as Africa’s trade with the rest of the world contracted.

Source: Source: China-Africa Economic Bulletin, 2026 Edition. Authors’ calculations from United Nations (2025).

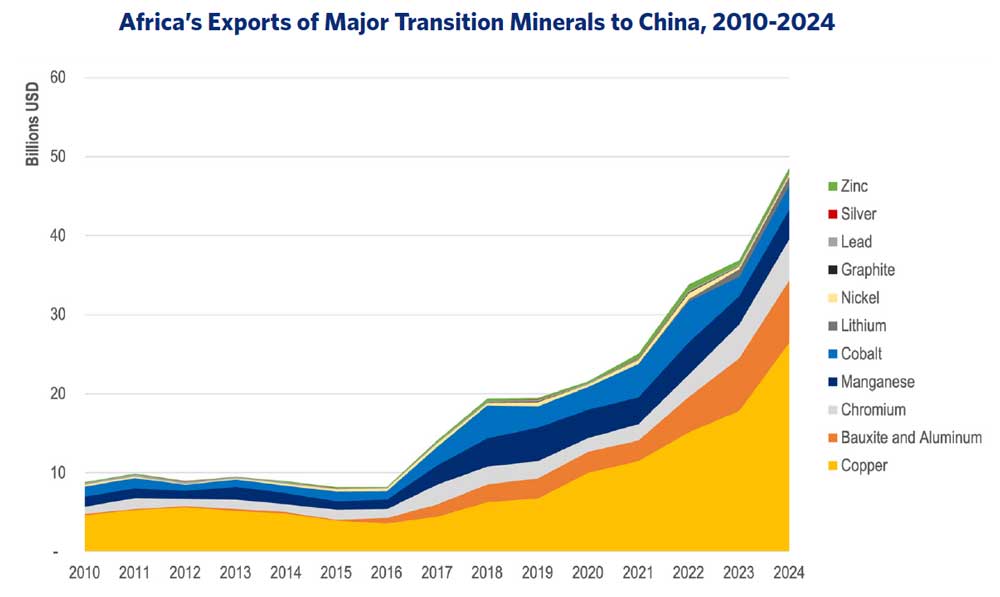

On the export side, the increase was driven primarily by extractives. This pattern is not new. For two decades, extractive products like iron ores, petroleum oil, copper and aluminum have dominated Africa’s exports to China, with agriculture and manufacturing each accounting for less than 10 percent of total trade value.

What has changed, however, is the growing importance of transition minerals within that extractive basket. Since 2020, copper exports have accelerated from the Democratic Republic of Congo including ores, concentrates and refined products.

Guinea’s bauxite and aluminum exports have followed a similar trajectory. The continent also supplies over 80 percent of China’s global imports of chromium and manganese ores and concentrates, primarily exported from South Africa.

Source: China-Africa Economic Bulletin, 2026 Edition. Authors’ calculations from Asian Development Bank, World Trade Organization (2024) and United Nations (2025). Note: China’s import data were used instead of the partner country’s export data due to data availability.

China’s recent zero-tariff policy is likely to lift volumes of products Africa already exports rather than diversify the continent’s export basket. Without complementary industrial policies, the trade deficit––currently equal to 3.1 percent of Africa’s regional GDP––could widen further.

China Shapes Africa’s Energy Transition Through Trade and Construction Contracts

China has made tangible commitments to Africa’s energy transition, but these engagements are occurring primarily through trade and construction contracts rather than lending or equity investment at meaningful scale.

China’s exports of low-carbon technology (LCT) goods to Africa reached $9.8 billion in 2024, this includes solar modules, batteries, electric vehicles and pollution control equipment. This represents 5.4 percent of total Chinese exports to the continent, more than double the LCT exports in 2013 (less than $4 billion).

The bulk of these flows in 2024 went to Africa’s largest economies with biggest power markets including South Africa, Nigeria, Egypt, Morocco and Algeria.

However, the rapid growth of China’s LCT exports has likely been driven by low prices supported by export rebate policies. That dynamic could change as China has begun phasing out value-added tax export rebates on solar modules and reducing rebates on batteries starting April 2026.

By contrast, China’s financial flows to Africa’s energy sector have remained limited. While no new Chinese FDI or lending to fossil fuels has been recorded in Africa since 2021, cumulative Chinese lending to non-hydro renewables (solar, wind, nuclear and geothermal) across the continent totaled only $1.7 billion between 2000 and 2024.

Verified FDI in renewable projects in 2023 and 2024 amounted to roughly $200 million, spread across small-scale wind, solar, and geothermal projects in Kenya and Namibia.

More than 70 percent of Chinese renewable energy engagement in Africa from 2022 to 2025 took the form of engineering, procurement and construction (EPC) contracts, a higher share than Asia and Europe where equity investments are more common.

The reliance on EPC model offers Chinese firms lower risks and faster revenue returns, but it reflects a shortage of bankable projects in Africa that could attract Chinese equity investors. This underscores the need for prefeasibility facilities to unlock the pipeline of renewable projects in Africa.

Technical assistance and grant programs, such as the Africa Solar Belt program announced at the 2023 inaugural Africa Climate Summit, have reached a broader group of African countries and offer valuable knowledge transfer and local training. However, they are not a substitute for the concessional lending that has historically catalyzed private sector participation or FDI.

President Bola Tinubu announced on May 13 that Nigeria will spend $11.6 billion on debt servicing in 2026, almost half of its projected government revenue. Many other African countries face the same challenge in debt repayments.

As the net transfers from China to African countries turn negative, meaning that Africa is due to pay more money back than the amount of loans it receives from China, the financing gap risks sidelining critical spending on climate resilience and energy transition.

No single “China in Africa”: African policy Also Shapes the Relationship

This latest data suggests that China-Africa economic interaction is country-specific rather than monolithic, and that African governments play a visible role in shaping outcomes.

This is evident through the influence host-country industrial strategies have on Chinese FDI. For example, the recent surge in Chinese electric vehicle and battery investment in Morocco reflects Morocco’s preferential trade access to the U.S. and EU markets and its supportive industrial policies. Egypt has likewise attracted Chinese investment in industrial parks, textiles and green hydrogen in line with its own strategy.

Trade policy decisions within African countries can also influence FDI. Zimbabwe’s 2022 ban on raw lithium ore exports coincided with Chinese investment in lithium concentrator facilities in 2022 and 2023. Though many Chinese companies were not impacted by the export ban; the subsequent tightening of that policy in 2026, which extended the ban to lithium concentrates, catalyzed a further round of Chinese investment in lithium sulfate processing plants.

Energy lending data in the past two decades also demonstrates a similar pattern that reflects host countries’ priorities. Oil-related lending has recurred in Angola, South Africa and Sudan; hydropower has concentrated in Ethiopia, Zambia and Uganda; wind projects have clustered in Ethiopia; and solar and geothermal in Kenya.

These trends point to substantial heterogeneity rather than a uniform greening trajectory across the continent.

The 2024 data points to a China-Africa economic relationship in evolution rather than transformation. The trends also point to growing differentiation across countries: Chinese FDI increasingly concentrated in North Africa driven by industrial policy and trade access to wider markets; export growth in countries rich in transition minerals that anchor China’s clean energy supply chains.

At the same time, African governments are taking visible initiatives to shape the relationship, such as Zimbabwe’s lithium export controls on raw minerals to catalyze domestic processing and value addition.

Moving forward, a continent-wide policy from China will more likely produce country-specific outcomes. It is important for both sides to be creative in deploying new tools, including local-currency and RMB trade finance, prefeasibility facilities that build a pipeline of bankable renewable energy projects, or industrial policies to attract Chinese FDI. Whether Chinese engagement in Africa translates into desired economic results will depend as much on Africa as on the scale and composition of what China offers.

Mengdi Yue is a research fellow at the Boston University Global Development Policy Center (GDP Center).